High oil prices, now above $100 per barrel, function as a levy on consumers and businesses. They boost inflation, deplete disposable income, and threaten economic growth. If sustained, job losses may follow.

Ryan Nunn, Director of Research at Yale University’s Budget Lab, addressed the impact on the U.S. economy—specifically on consumer goods—as the conflict with Iran unfolds and prices for these goods subsequently rise; he acknowledged that oil markets have swung sharply between panic and relief since the outbreak of the war in the Middle East, even as they brace for increased volatility.

Nunn’s insights connect to the broader economic impact, as he addresses how the ongoing conflict with Iran and the resulting surge in oil prices specifically affect consumer goods in the U.S. economy.

Nunn observes that oil markets have repeatedly oscillated sharply between panic and calm since the onset of the war in the Middle East, suggesting heightened volatility.

He notes that, drawing from macroeconomic research—including his own and that of others—on the predicted effects of turbulence in the energy market, it remains challenging to assess the actual scale of this oil shock, and even more difficult to forecast its economic consequences.

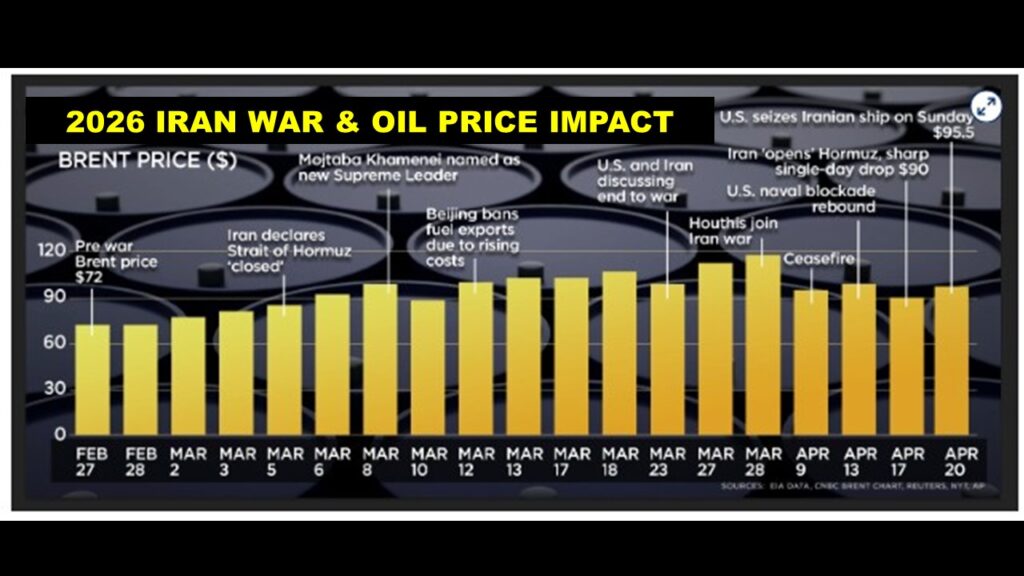

Prices have soared by more than 55% since the war began. Brent crude climbed from about $72 per barrel on February 27 to nearly $120 at its peak, as anxiety grew over possible supply disruptions through the Strait of Hormuz. Brent crude rallied 51% in March, marking one of the largest monthly price jumps in oil history.

Nunn acknowledges that this is one of the largest increases in U.S. oil prices in 50 years. The subsequent decline suggests prices may pull back slightly.

Consumers are feeling the impact at the gas pumps.

When oil prices surge, gasoline prices and inflation rise. Prices increase, and economic activity slows.

As of April 24, Georgia had the lowest gasoline price per gallon at $3.582. Hawaii ($5.649) and California ($5.884) had the highest figures.

Understanding History

The Director of Research at Yale University’s Budget Lab says it is essential to examine the United States’ experience with other oil price shocks to understand today’s instability.

He explained that researchers must do more than observe the ‘before and after’ of historical crude oil price fluctuations. A booming economy can cause oil prices to rise due to increased demand, not supply.

They adopted a methodological design proposed by Diego Kanzig, focusing on a narrow time window around OPEC announcements. This aims to isolate price variations caused by supply contractions, excluding other phenomena.

Assume this $35-per-barrel price shock persists for a full quarter. Based on about 20 years of data, our study suggests that, one year later, core price levels could rise by just under 0.5%. GDP could contract by just under 0.5%.

Though this may seem small, U.S. GDP is roughly $30 trillion. This means a reduction in output of about $115 billion over the course of a year. Still, oil price shocks now have less severe impacts on the U.S. than before.

Nunn notes, ‘Effects remain significant, but less so than before.’ These effects are smaller now because the United States requires less oil to generate a dollar of GDP. Improved fuel efficiency and shifts away from oil-intensive sectors have reduced dependence on oil.

Ryan Nunn, Director of Research at Yale University’s Budget Lab.

The United States now produces much more oil and is a net exporter of crude and petroleum products. As crude prices rise, more offsetting effects emerge and balance out; investment increases over time, partially offsetting the decline in consumption from price hikes.

In essence, this constitutes the general macroeconomic landscape.

Consumer Inflation

But what does all this mean for consumers? And how does inflation affect different people in different ways?

Generally, this type of inflationary shock hits low-income households hardest. They spend a larger share of their budget on goods, cannot easily substitute cheaper products, and have smaller savings.

Nunn stated, ‘If we analyze spending by low- and high-income households, it is reasonable to expect this energy shock will generate higher inflation for low-income households. They spend more on energy, relative to total consumption.’

“Similarly, they are more vulnerable to any unemployment increase arising from an economic slowdown, if one occurs; and focusing on oil supply contractions, various studies show these hits fall harder on households with lower education levels than on others,” he added.

However, stepping back to assess the nature of the economic impact now experienced in the United States and globally, both duration and uncertainty are crucial—not just the magnitude of initial shifts. Thus, outcomes depend heavily on how long the war lasts and how rapidly production and trade recover after the initial disruption.